Quick Take

- Microsoft, EA, and Sony scale back projects and teams as revenue growth turns negative

- Post-pandemic boom period fades, exposing long-term cost and production challenges

- Industry pivots from aggressive expansion to leaner, more sustainable distribution models

At the upper end of the video game market, a broad recalibration is now underway. Microsoft, Electronic Arts, and Sony have each initiated significant workforce reductions, shelved projects, and shifted strategic priorities as the long-predicted slowdown in growth reaches the industry’s largest firms.

Microsoft is reportedly preparing for major layoffs within its gaming division, according to internal sources. Managers across Xbox are expecting job losses to affect nearly every part of the organization. The move follows a series of announcements this month, including the unveiling of a handheld device, a collaboration with AMD, and an extended partnership with Meta to launch the Xbox Edition of Meta Quest 3S. Microsoft is also deprioritizing its HoloLens and proprietary hardware development in favor of a software-first strategy focused on services and platforms.

Electronic Arts confirmed layoffs across multiple teams in May, including developers at Respawn Entertainment. The publisher also canceled its planned Black Panther title. These decisions came after EA reported $7.5 billion in net revenue for its fiscal year ending March 2025, a 1.3% drop from the previous year. Live services continued to generate most of the company’s income, but even those saw minimal growth.

Sony made similar cuts, eliminating roughly a third of the staff at Bend Studio. The decision followed the cancellation of an unannounced live service game. Across the board, the three largest platform holders are reducing their exposure to costly, long-cycle development and large-scale production teams.

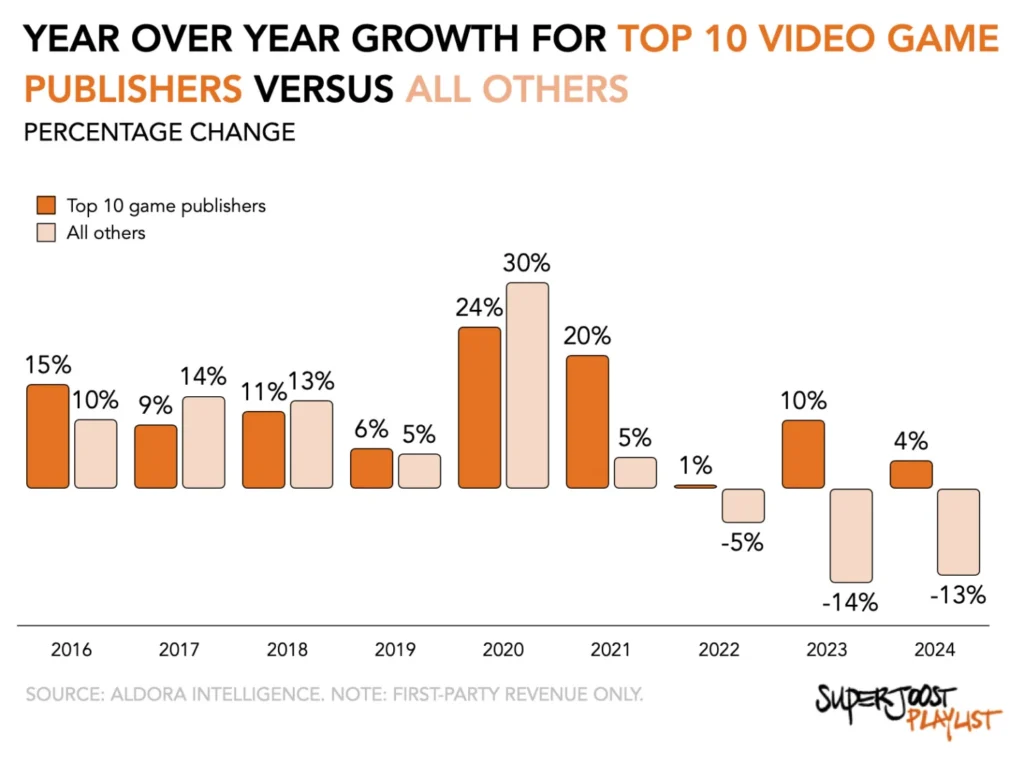

The shifts are part of a broader trend. From 2016 through 2020, the largest ten video game publishers consistently grew faster than the rest of the market. Pandemic-era demand in 2020 drove top-10 revenue up by 24%, compared to a 30% rise for smaller publishers. But growth at the top has slowed sharply since then. In 2022, major publishers plateaued while smaller firms dipped into negative territory. In 2023, the larger firms regained ground with a 10% revenue increase, but smaller studios declined further, down 14%. By 2024, the performance gap narrowed again, with both segments showing limited movement.

This contraction reflects structural changes. The era of growth through acquisition and escalating production budgets is giving way to a more restrained approach. Rather than pushing content volume, firms are emphasizing distribution models, recurring engagement, and more efficient development pipelines. Analysts have framed the current market as a correction rather than a collapse, with large companies now facing the same economic pressures that hit mid-sized developers in 2023.

The result is a reset in expectations. High output, high headcount studios are now being reshaped into leaner operations built for long-term sustainability. The assumption that market share and intellectual property would continue delivering consistent returns has weakened. The largest publishers are moving into a phase defined less by dominance and more by adaptation.

Source: SuperJoost